1800-270-7000

1800-270-7000

Basics of Derivatives

Basics of Derivatives

A derivative is a contract or a product whose value is derived from the value of some other asset known as the underlying. Derivatives are based on a wide range of underlying assets.

- Petrol

- Diesel

- Kerosene

- Curd

- Paneer

- Buttermilk

In both examples, the value of the derivative product is linked to the value of the underlying asset. Changes in the underlying asset directly influence the derivative.

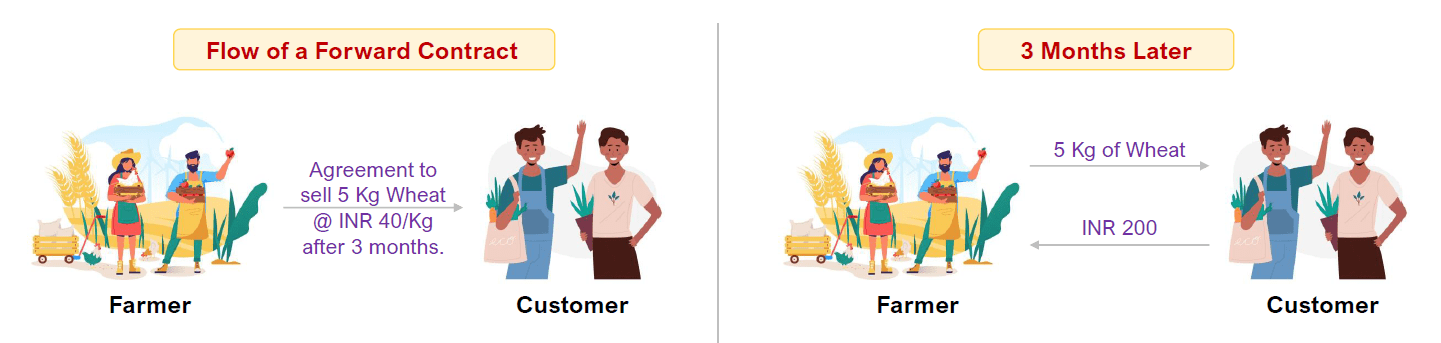

Forward Contract

Forward Contract

Essential features of a forward contract are:

- It is a contract between two parties (Bilateral contract).

- All terms of the contract like price, quantity and quality of underlying, delivery terms like place, settlement procedure etc. are fixed on the day of entering into the contract.

Major Limitation of Forward Contracts

Liquidity Risk

Liquidity refers to the ability of the market participants to buy or sell the desired quantity of an underlying asset. As forwards are tailor-made contracts i.e. the terms of the contract are according to the specific requirements of the parties, other market participants may not be interested in these contracts.

Counterparty Risk

Counterparty risk is the risk of economic loss arising from the failure of a counterparty.

Market Participants

Market Participants

1. Hedgers

Entrepreneurs, corporations, investing institutions and banks all use derivative products to hedge or reduce their exposures to market variables such as interest rates, share values, bond prices, currency exchange rates and commodity prices.

2. Traders/Speculators

Try to predict the future movements in prices of underlying assets and based on the view, take positions in derivative contracts. Derivatives are preferred over underlying asset for trading purpose, as they offer leverage, are less expensive (cost transaction is generally lower than that of the underlying) and are faster to execute in size (high volumes market).

3. Arbitrageurs

Originates when a trader purchases an asset cheaply in one location and simultaneously arranges to sell it at a higher price in another location. Such opportunities are unlikely to persist for very long, since arbitrageurs would rush into these transactions, thus closing the price gap at different locations.

Significance of Derivatives

Significance of Derivatives

It helps in improving price discovery based on actual valuations and expectations.

It enables the transfer of various risks from those who are exposed to risk but have a low risk appetite to participants with a high-risk appetite. For example, hedgers want to give away the risk whereas traders are willing to take risk.

It enables the shift of speculative trades from the unorganized market to the organized market. Risk management mechanism and surveillance of activities of various participants in the organized space provide stability to the financial system.

Practice Questions

Practice Questions

Question 1

___________________ wants to make money at all the time regardless of any fluctuations happening in the market.

- Straddle

- Hedger

- Speculator

- All of the above

Show Answer

Question 2

What does hedging do?

- It maximises business profits

- It minimises business losses

- It produces a clearer outcome

- Hedging can be used only in currency markets and not in equity markets

Show Answer

Hedging is a risk management strategy used by businesses or investors to reduce the potential adverse effects of price movements in financial markets.

Analogy: Amazon Shopping vs Stock Market

Analogy: Amazon Shopping vs Stock Market

| Amazon Shopping | Stock Market |

|---|---|

| Buyer: Click 'Buy' | Buyer places Buy order |

| Seller: Click 'Sell' (he has the product) | Seller places Sell order (he has the shares) |

| Order details sent to Amazon system | Trade details sent to Clearing Corporation |

| Amazon checks if seller has stock | Depositories confirm seller has shares to Clearing Corporation |

| Product moved to Amazon warehouse | Seller’s shares moved to a pool account (temporary holding) to be ready for delivery |

| Final stock balance check | Depository does a final check to avoid errors and confirms final balance |

| Amazon adjusts orders/returns (netting) | Clearing Corp nets out broker’s trades. Example: Buy 1,000 shares, Sell 600 shares = only 400 need to be settled |

| Buyer pays and gets delivery | Funds and shares exchanged (Pay-in/Pay-out). On settlement day (T+1 or T+2): Buyers’ brokers pay money; Sellers’ brokers deliver shares |

| Amazon: 'Order delivered successfully’ | Clearing & Settlement completed. Clearing Corporation ensures money goes to sellers and shares go to buyers |

| Amazon is middleman between buyer and seller | Clearing Corp acts as counterparty (Novation) |

| If seller fails, Amazon finds another seller/refunds | If seller defaults, Clearing Corp holds auction/compensates. If seller fails, Clearing Corporation buys shares from the market (auction) or compensates the buyer |

Legal and Regulatory Framework

Legal and Regulatory Framework

Securities Contracts (Regulation) Act, 1956 (SCRA)

Governs stock trading and aims to prevent market manipulation.

SEBI Act, 1992

Establishes the Securities and Exchange Board of India (SEBI) to regulate and protect investors.

Practice Questions

Practice Questions

Question 1

What does novation mean in the context of trade clearing?

- The clearing corporation becomes the legal counterparty to both sides of every trade.

- Modification of an order before it is executed on the exchange.

- Cancellation of unsettled trades at the end of the day.

- A penalty charged by the exchange for default.

View Solution

Question 2

What is multilateral netting as performed by the clearing corporation?

- Consolidating all trades of all clearing members to determine net delivery and payment obligations for each member, rather than settling trade-by-trade.

- Offsetting buy and sell orders before trade execution on the exchange.

- Pairing each buyer with a single specific seller for delivery (bilateral netting only).

- Netting off a broker’s losses in one security against profits in another security for margin benefit.

View Solution

Question 3

A Clearing Member has to deposit ______________ to clearing corporation which forms part of the security deposit.

- Rs. 50 Lakhs

- Rs. 100 Lakhs

- Rs. 150 Lakhs

- Rs. 20 Lakhs

View Solution

Clearing Member Eligibility Norms • Net-worth of at least Rs.300 lakhs. The Net-worth requirement for a Clearing Member who clears and settles only deals executed by him is Rs. 100 lakhs. • Deposit of Rs. 50 lakhs to clearing corporation which forms part of the security deposit of the Clearing Member. • Additional incremental deposits of Rs.10 lakhs to clearing corporation for each additional TM, in case the Clearing Member undertakes to clear and settle deals for other TMs.

Quick Comparison: Forwards vs Futures

Quick Comparison: Forwards vs Futures

| Feature | Forwards | Futures |

|---|---|---|

| Trading | Private (OTC) | Exchange Traded |

| Customization | Fully Customizable | Standardized |

| Counterparty Risk | High | Low (Clearing House) |

| Settlement | At Expiry | Daily Mark-to-Market |

| Liquidity | Low | High |

| Settlement | Delivery | Cash Settled |

| Underlying | Commodities, Oil, Agriculture, Currency | Equity Stocks, Equity Index, Currency, Interest Rates |

| Price Discovery | Less Transparent | Transparent via Exchange |

Future - Long and Short Pay-off in a nut-shell

Future - Long and Short Pay-off in a nut-shell

| Strategy | Right/Obligation | Market View (Expectation) | Profit Potential | Loss Potential | Premium Involved | Margin Required |

|---|---|---|---|---|---|---|

| Futures Buy (Long) | Obligation to buy at agreed price | Bullish (Expect ↑) | Unlimited | Unlimited | No | Yes |

| Futures Sell (Short) | Obligation to sell at agreed price | Bearish (Expect ↓) | Unlimited | Unlimited | No | Yes |

Meaning of Margin

Meaning of Margin

Margin is the sum that is blocked from our account when we open a derivatives position. Formula

Components of Initial Margin

SPAN Margin

SPAN (Standard Portfolio Analysis of Risk) Think of it as a risk calculator used worldwide. It looks at your entire portfolio and figures out: “If the market moves badly tomorrow, how much can you lose?” Based on this, it decides how much margin (deposit) you must keep.

Exposure Margin

This adds an extra buffer-against sudden, wild swings. For stock futures and option selling, it’s approximately 3.5% of the contract value. For index derivatives, it's around 2-3%.

Example (Nifty Futures, Lot Size = 75)

Day 1: Entry

Buy Nifty futures at ₹17,800. Contract value = ₹17,800 × 75 = ₹13.35 lakh.

Margin blocked (say 12%) = ₹1.6 lakh.

Closing price = ₹18,000.

Gain = (18,000 – 17,800) × 75 = ₹15,000.

Profit added → Margin balance rises to ₹1.75 lakh.

Day 2

Reference = 18,000. Closing = ₹17,900.

Loss = (17,900 –18,000) ×75 = -₹7,500.

Loss deducted → Margin balance falls to ₹1.675 lakh.

Day 3

Reference = 17,900. Closing = ₹18,100.

Gain = (18,100 – 17,900) × 75 = ₹15,000.

Profit added → Margin balance becomes ₹1.825 lakh.

Futures Pricing

The Cash and Carry Model explains that the futures price equals the spot price plus the cost of carry minus any income from the asset (like dividends).

F = Futures Price

S = Spot Price

This is the basic version, used when costs/income are expressed in rupee terms or using simple interest.

Practice Questions

Practice Questions

Question 1

Which of the following statements best distinguishes a forward contract from a futures contract?

- Forwards are standardized contracts traded on exchanges, while futures are private agreements traded over-the-counter.

- Forwards settle gains/losses only at maturity, whereas futures are marked-to-market daily with margins.

- Forwards carry minimal credit risk due to clearinghouse guarantees, whereas futures have high counterparty default risk.

- Forwards require an initial margin deposit, while futures typically require no upfront payment.

View Solution

Question 2

Suppose the spot price of a stock index is ₹10,000. The risk-free interest rate is 6% per annum. Assume no dividends on the index and no other holding costs or benefits. What is the fair futures price for a contract expiring in 6 months (0.5 year), based on the cost-of-carry model? (Use simple interest for approximation.)

- ₹10,000

- ₹10,300

- ₹10,600

- ₹10,700

View Solution

Question 3

Mr. Sharma shorts 1 lot of XYZ futures at ₹200 per unit. Each lot represents 100 units. Later, he closes (squares off) his position at ₹180 per unit. What is Mr. Sharma’s profit or loss on this futures trade (ignoring transaction costs)?

- ₹2,000 profit

- ₹2,000 loss

- ₹20 profit

- ₹20 loss

View Solution

• A short futures position profits when prices fall.

• Mr. Sharma sold at ₹200 and bought back at ₹180, gaining ₹20 per unit. With a lot size of 100 units, his total profit = ₹20 × 100 = ₹2,000. This is a realized profit added to his account.

Question 4

If a trader’s futures position incurs losses such that the funds in the margin account fall below the required maintenance margin level, what typically happens?

- The trader will receive a margin call to deposit additional funds to restore the margin to the initial level.

- The position is automatically terminated by the exchange with no further action.

- The trader can continue to hold the position until expiry without adding funds.

- The losses are ignored as long as the trader has paid initial margin once.

View Solution

What are OPTIONS?

What are OPTIONS?

A Contract that:

- Gives the buyer the right, but not the obligation; To buy or sell a specified underlying asset; at a set price on or before a specified date

Types of OPTIONS Contract

| Buyer | Seller |

|---|---|

|

CALL Has the right to buy a stock at specified price |

CALL Has the obligation to sell a stock at a specified price |

|

PUT Has the right to sell a stock at specified price |

PUT Has the obligation to buy a stock at specified price |

Options Terminology

These options have a stock index as the underlying asset. For example, Options on Nifty, Sensex, etc.

These options have individual stocks as the underlying asset. For example, Option on ONGC, NTPC, etc.

The owner (buyer/holder) of an American Option can exercise his right at any time on or before the expiry date/day of the contract.

The owner (buyer/holder) of a European Option can exercise his right only on the expiry date/day of the contract. In India, all Index and Stock Options are European Style Options.

It is the price which the option buyer pays to the option seller.

It is the price at which the underlying asset is trading in the spot market. In our examples, it is the value of underlying index (Nifty 50) which was 18315.10 at that point of time.

Strike price is the price per share for which the underlying security may be purchased by the call option holder (or sold by the put option holder). In our examples, strike price for both call and put options is 18400.

Moneyness of an Option

In-the-money (ITM) Option

This option would give the option holder a positive cash flow, if it were exercised immediately. A call option is said to be ITM, when spot price is higher than strike price. A put option is said to be ITM when spot price is lower than strike price. In our examples, the put option is in-the-money.

At-the-money (ATM) Option

At-the-money option would lead to zero cash flow if it were exercised immediately. Therefore, for both call and put ATM options, strike price is equal to spot price. In reality, because the strike prices are at fixed intervals of say, Rs.5, Rs.10 or Rs.50, while the spot price moves in much smaller increments, the two prices may rarely be equal. Hence an ATM option can be defined as an option with a strike price which is closest to the spot price.

For example, if the index is at 18415 and three options on the index with strike prices of 18350, 18400 and 18450 are available for trading, the option with the strike price of 18400 is an ATM option.

Out-of-the-money (OTM) Option

An out-of-the-money option is one with a strike price worse than the spot price for the holder of option. In other words, this option would give the holder a negative cash flow if it were exercised immediately.

An out-of-the-money option is one with a strike price worse than the spot price for the holder of option. In other words, this option would give the holder a negative cash flow if it were exercised immediately. A call option is said to be OTM, when spot price is lower than strike price. A put option is said to be OTM when spot price is higher than strike price. In our examples, the call option is out-of-the-money.

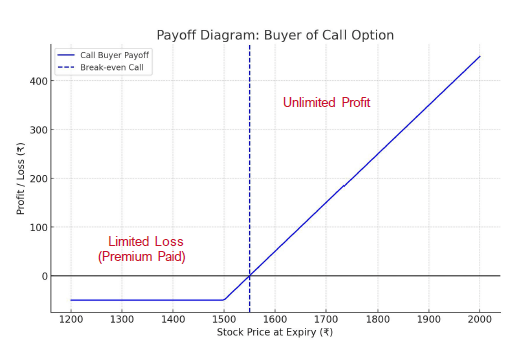

Call Option – Right to Buy & Put Option – Right to Sell

Call Option – Right to Buy & Put Option – Right to Sell

Call Option – Right to Buy

A Call option gives the buyer the right (not obligation) to buy an asset at a fixed price (called Strike Price) before/at expiry.

The seller (writer) of the call is obligated to sell if the buyer chooses to exercise.

The buyer pays a Premium to the seller.

Premium is like a booking fee.

Call Buyer (Right to Buy at ₹1,500. Premium ₹50)

- Loss is limited to premium (₹50) → flat line below zero.

- Profit starts after ₹1,550 (Strike + Premium = Breakeven Price) and grows unlimited as stock price rises.

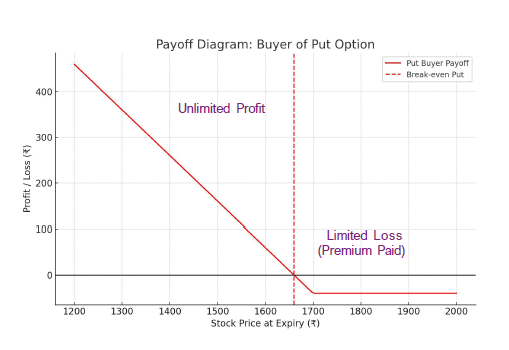

Put Option – Right to Sell

A Put Option gives the buyer the right (not obligation) to sell an asset at strike price before/at expiry.

The seller (writer) of the put must buy if the buyer exercises.

Buyer pays premium, risk is limited, and the seller receives the premium.

Buying a Put Option Profitability depends on the Concept of Selling High at price and Buying at a Low price.

Put Buyer (Right to Sell at ₹1,700, Premium ₹40)

- Loss is limited to premium (₹40) → flat line below zero.

- Profit starts after ₹1,660 (Strike Premium = Break even) and increases as stock price falls.

In Short

| Call Option | Put Option |

|---|---|

| Call Buyer = Spot Price > Strike Price = Intrinsic Value | Put Buyer = Spot Price < Strike Price = Intrinsic Value |

| Intrinsic Value = Spot Price – Strike Price | Intrinsic Value = Strike Price – Spot Price |

| Example: Strike Price is Rs. 100; Spot Price is Rs. 200 | Example: Strike Price is Rs. 100; Spot Price is Rs. 50 |

| Intrinsic Value = 200 - 100 = Rs. 100 | Intrinsic Value = 100 - 50 = Rs. 50 |

| Assume Premium Paid by the Call Buyer is Rs. 20 | Assume Premium Paid by the Put Buyer is Rs. 20 |

| Profit =Rs. 100 –Rs. 20 = Rs. 80 | Profit =Rs. 50 –Rs. 20 =Rs. 30 |

| Break-even Price = Rs. 100 + Rs. 20 = Rs. 120 (Strike Price + Premium) | Break-even Price = Rs. 100 - Rs. 20 = Rs. 80 (Strike Price – Premium) |

| For a Call Seller, the maximum gain is the premium received, but loss is unlimited. | For a Put Seller, the maximum gain is the premium received (Rs. 20), but loss is unlimited. |

Quick Recap – Call and Put Option

Quick Recap – Call and Put Option

| Strategy | Right / Obligation | Market View (Expectation) | Profit Potential | Loss Potential | Premium Involved | Margin Required |

|---|---|---|---|---|---|---|

| Call Buy | Right to buy at strike price | Bullish (Expect ↑) | Unlimited | Limited (to premium paid) | Pay | No |

| Call Sell | Obligation to sell if buyer exercises | Bearish / Neutral | Limited (Premium received) | Unlimited | Receive | Yes |

| Put Buy | Right to sell at strike price | Bearish (Expect ↓) | Unlimited (if price ↓ significantly) | Limited (to premium paid) | Pay | No |

| Put Sell | Obligation to buy if buyer exercises | Bullish / Neutral | Limited (Premium received) | Unlimited | Receive | Yes |

Practice Questions

Practice Questions

Question 1

If you sell a put option with strike of Rs. 245 at a premium of Rs.40, how much is the maximum gain that you may have on expiry of this position?

- 285

- 40

- 0

- 205

View Solution

For a Put Seller, Gain is limited to premium received but the loss is unlimited.

Question 2

Spot Price = Rs. 100. Call Option Strike Price = Rs. 98. Premium = Rs. 4. An investor buys the Option contract. On Expiry of the Option the Spot price is Rs. 108. Net profit for the Buyer of the Option is _____________.

- Rs. 6

- Rs. 5

- Rs. 2

- Rs. 4

View Solution

As Spot Price > Strike Price; It is a gain for the Call Option Buyer. Gain = (108-98) - 4 = 10 - 4 = 6

Quick Recap

Quick Recap

Moneyness – Depicts profitability of the Option Contract.

It is always from the perspective of a Call Buyer and Put Buyer.

| Option Type | In the Money (ITM) | At the Money (ATM) | Out of the Money (OTM) |

|---|---|---|---|

| Call Option (Right to Buy) | Spot Price > Strike Price | Spot Price ≈ Strike Price | Spot Price < Strike Price |

| Put Option (Right to Sell) | Spot Price < Strike Price | Spot Price ≈ Strike Price | Spot Price > Strike Price |

Practice Questions

Practice Questions

Question 1

If in case of Put Buy, Spot Price < Strike Price then it means a person is in __________ situation.

- At the money

- In the money

- Out the money

View Solution

Question 2

In-The-Money option is ____________.

- An option with a negative intrinsic value

- An option which cannot be profitably exercised by the holder immediately

- An option with a positive intrinsic value

- An option with zero-time value