1800-270-7000

1800-270-7000-

Our Products

-

Self Care

- Downloads

- Learnings

- About Us

-

More

-

Shareholders

-

Shareholders

-

-

SIP Calculators

-

Shareholders

![]() IMPORTANT ALERT ! Beware of Fake AMC App, Online Impersonation & Scam WhatsApp Groups.

IMPORTANT ALERT ! Beware of Fake AMC App, Online Impersonation & Scam WhatsApp Groups.

ABC Solution

Loans

Insurance

Aditya Birla Sun Life AMC Limited

Aditya Birla Sun Life AMC Limited

The 3-way guide to riding every Market Wave

Mar 13, 2020

4 mins

5 Rating

Was it really a virus or vulnerability due to valuations that triggered such a sharp correction in risk assets post Covid 19 outbreak? Whatever the cause, the effect is that the speed of correction in risk assets is one of the fastest in history. For most investors, in Jan 20, it felt like India equity market is finally becoming broad based with a hope of good return at the end of a long wait, and today it feels like ‘oops, I should have sold all my equity investments a month back’.

As a sales professional and an investor, I know how difficult it is for now. Yet, as an asset management Company and a market observer, I know risk or volatility is inevitable. In fact, it’s only because of volatility that outsized returns are possible. The key for now is to hold fort and not lose conviction in the long-term potential of businesses and by extension equity investments. Isn’t it easier said than done when 3-year SIP returns for most equity funds in the industry is are negative? Yes, it is. Let me share 3 ways in which we can possibly deal with it:

Adjust the Focus:

Over 50% of India’s listed equity is held by promoters. What is the likely reaction of sound promoters to this equity correction? Most veteran promoters won’t let a good crisis go waste. Similarly, an equity investor is effectively a partner in the firm, and they should also behave alike. But most retail investors don’t! Those of us who overcome finite disappointments of this sharp correction but don’t lose infinite hope of equity in long term ultimately stand to make money. So, do stay put. Also, many people have been wondering off late whether returns from MFs are really worth its uncertainty? The answer lies in the question itself. Compared to direct bonds and direct equity where there is a chance of huge or all loss of capital itself, MFs are judged basis return on capital rather than return of capital, over a period of time. Even today, 10- and 15-year SIP returns of Aditya Birla Sun Life Equity Fund and Aditya Birla Sun Life Large Cap Fund are 12.91% & 13.02% and 10.31% & 12.47% respectively. Whether you are an advisor or have an advisor, remember that a good advisor is one who does not only care for what the clients feels, but instead gives the clients what they need.

Asset Allocation:

This pill is a panacea in investing - the only antidote to weather the risk and realise the return potential in the market, over a complete cycle. As a matter of fact, about 90 Individual Financial Advisors in India have 500cr or higher AUM; and 60% of their AUM is in Debt. And yet, it’s so surprising that over 90% IFAs in India have over 85% of their AUM in Equity alone (Data Source: CAMS, Internal Research). This gap needs to be bridged, more so in the face of falling deposit rates. I believe Debt as an asset class is hugely underutilized for designing complete investment solution to MF investors in India. The key is to apply asset allocation across asset classes and also within asset classes (In equity, across: Multi cap, Large Cap, Mid / small cap, Sectoral / thematic. In Debt, across: Credit, Mid credit and top credit). Also, SIP Units have off late become the new Gold – investors look forward to accumulate units like what they used to do in Gold. It would be a grave mistake to, therefore, stop their SIPs now. Finally, we can, today, get loans for every financial need or goal but not for one - retirement. We, Indians, don’t have social security, and with growing life expectancy, health care costs are going up. Not building a retirement portfolio, would, thus, be the biggest mistake of a lifetime.

Adopt Money Advisory v/s Investment only Advisory:

Why do clients leave advisors? Research suggests that clients leave their advisors because the adviser has not developed a bond with them. Some clients leave because the advisor hasn’t communicated often enough or with a lop sided advisory. Clients mostly do not leave due to investment underperformance, even if in certain cases they say they do for this reason. This research offers a huge insight - advisors often limit themselves to being advisors for a product – mutual funds, insurance, loan etc. This is an inside out view. What clients understand is the language of money; products is an intermediary’s language. I urge our advisors to transition, if they have not already, from being Investment Only Advisors to being Money Advisors.

From valuations perspective, Bond yield minus earnings yield gap has become negative which is the largest gap since 2008 Global Financial Crisis. Historically, when the gap has turned negative (it means equities are more attractively valued than bonds), it presents a buying opportunity for equities (1 year forward returns are usually very attractive). Markets may fall more because during panic/ risk aversion, valuations can fall to irrational levels, but it presents an opportunity to start going overweight in equity allocation, and definitely not redeem.

Finally, for those who are questioning the above hope and investment appeal in the face of very low economic and earnings growth in recent years, remember that every decade, we have seen a few years when India GDP has grown at less than 5%. It does come back. So, don’t panic. Structural forces of demography, demand and cost & skill arbitrage are well in place to make it directionally irreversible. It generally comes back sooner than what people expect at this stage of economic and market cycle.

So, don’t lament that you didn’t sell your equity investments a month back. A year from now, history says you’ll be glad you didn’t.

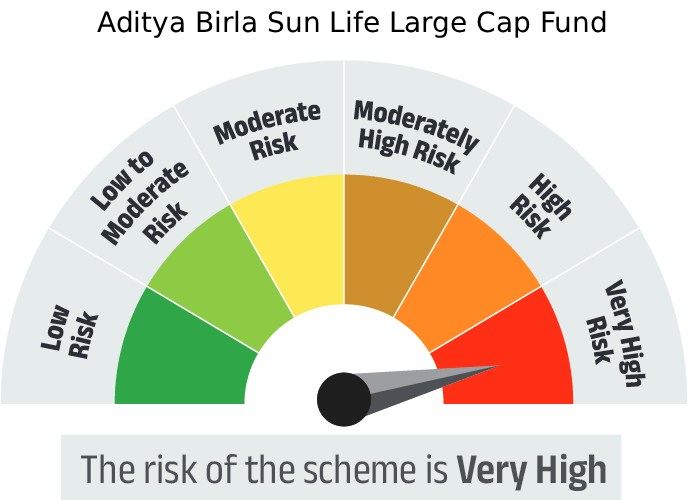

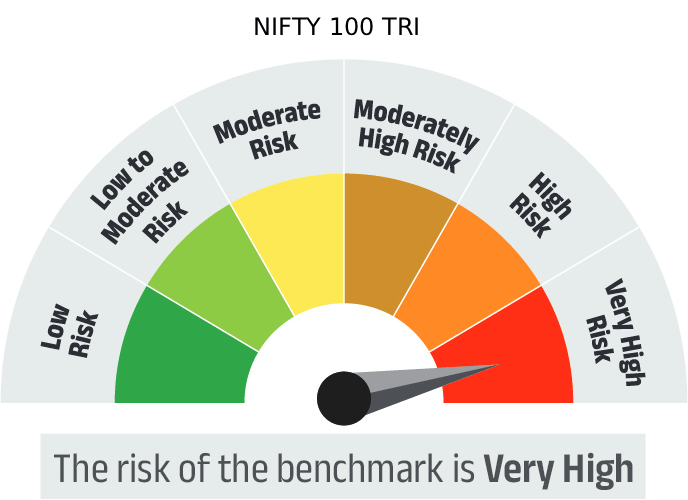

| Scheme Name | This product is suitable for investors who are seeking* | Risk-o-Meter | Benchmark Risk-o-Meter |

|---|---|---|---|

Aditya Birla Sun Life Large Cap Fund |

|

|

|

| *Investors should consult their financial advisers if in doubt about whether the product is suitable for them. | |||

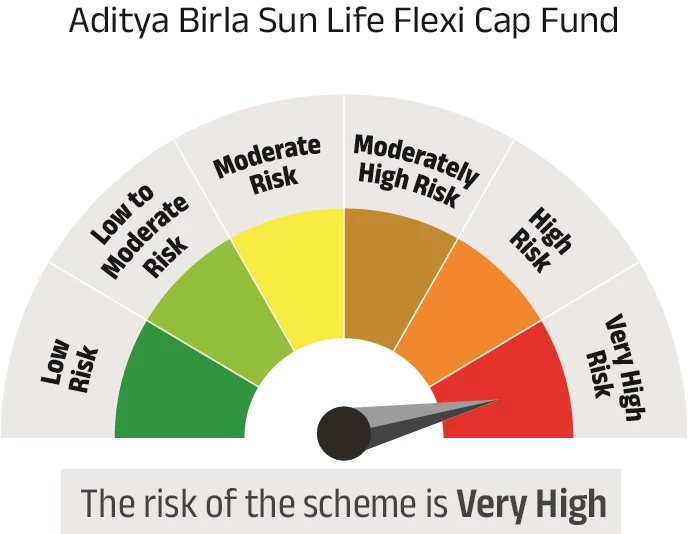

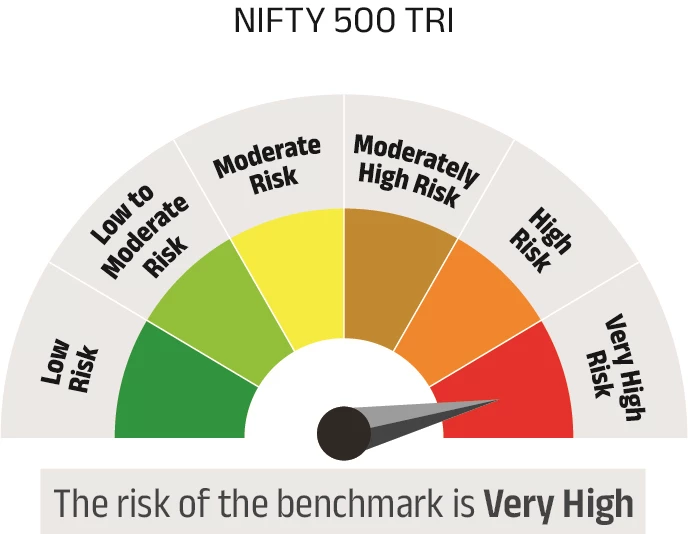

| Scheme Name | This product is suitable for investors who are seeking* | Risk-o-Meter | Benchmark Risk-o-Meter |

|---|---|---|---|

Aditya Birla Sun Life FlexiCap Fund |

|

|

|

| *Investors should consult their financial advisers if in doubt about whether the product is suitable for them. | |||

For the schemes’ full performance table please refer latest empower. Past performance may or may not be sustained in future. For further details please refer SID/KIM of the schemes.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.