1800-270-7000

1800-270-7000-

Our Products

-

Self Care

- Downloads

- Learnings

- About Us

-

More

-

Shareholders

-

Shareholders

-

-

SIP Calculators

-

Shareholders

![]() IMPORTANT ALERT ! Beware of Fake AMC App, Online Impersonation & Scam WhatsApp Groups.

IMPORTANT ALERT ! Beware of Fake AMC App, Online Impersonation & Scam WhatsApp Groups.

ABC Solution

Loans

Insurance

Aditya Birla Sun Life AMC Limited

Aditya Birla Sun Life AMC Limited

Plan for Life: Build Your Own Monthly Paycheck with SIP & SWP

Nov 24, 2025

5 min

0 Rating

You know that feeling when your phone buzzes and you see, “Salary credited”?

It’s not just money. It’s peace of mind.

It fuels your dreams, pays your bills, and gives your routine a reassuring rhythm. It becomes the steady heartbeat of your financial comfort.

However, there is one simple rule it always follows. It shows up only when you do.

The moment you take a sabbatical, a break, or even retire, that comforting "Salary Credited" message disappears.

Now, imagine if your money could do what you do every month. Imagine it showing up reliably on the first of every month.

There would be no need for a manager or an appraisal cycle. Your investments would quietly send you your own "Amount credited” Notification.

Does this sound too good to be true?

It is not. When we say ‘Plan for Life’ it means with the combined power of Systematic Investment Plans (SIP) and Systematic Withdrawal Plans (SWP), you can build your own monthly paycheck. This paycheck does not rely on anyone else. It depends entirely on the smart financial steps you take today.

Here is how it works:

SIP: your wealth builder

A Systematic Investment Plan (SIP) is like your financial career in motion. Your money works just as hard and just as consistently as you do.

SIPs allow you to invest small, manageable amounts in mutual funds on a regular basis, usually monthly. This investment pattern aligns perfectly with your income cycle. It is an automated and disciplined approach to investing that turns consistency into your greatest advantage.

Why SIPs are a great starting point?

You can begin with small, manageable monthly investments.

The process is automated, which makes it easy to stay consistent.

You can align your SIP date with your salary credit day.

You can increase your SIP amount as your income grows.

You benefit from rupee cost averaging, helping you manage market volatility.

Over time, compounding adds significant value to your investments.

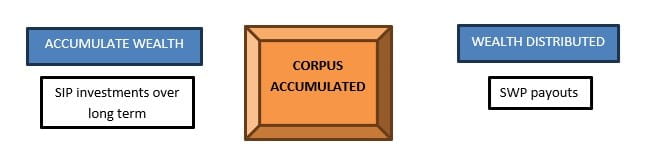

This phase is where your wealth starts taking shape. SIPs help you grow your money silently in the background while you focus on life.

SWP: Your Wealth Distributor

If SIPs represent the years when you build wealth, then Systematic Withdrawal Plans (SWP) are for the time when your investments begin to pay you back. As you approach retirement or decide to slow down, you can shift your accumulated SIP corpus into more stable investments. These can include debt or hybrid mutual funds that offer lower volatility while continuing to generate returns. SWPs allow you to withdraw a fixed amount from your investments at regular intervals. These intervals can be monthly, quarterly, or yearly. This gives you a reliable income stream from the wealth you have already built.

Why SWPs are a smart payout strategy?

You can choose how much money you want to receive and how often.

Your remaining corpus stays invested and continues to earn returns.

Your cash flows are regular, predictable, and fully under your control.

You can enjoy a self-funded pay check like a salary credit.

You continue to benefit from potential market gains even as you withdraw money.

This approach supports a peaceful and financially secure retirement or career break.

SWP gives you the freedom to live on your terms. It helps you maintain your lifestyle without depending on anyone else to pay you. Hence, you Plan for Life with SIP + SWP strategy.

Together: A lifetime income framework

When combined, SIPs and SWPs form a powerful financial lifecycle.

During your working years, SIPs help you build wealth consistently.

When you are ready to start a second income or retire, SWP turns that wealth into a reliable, inflation-beating income.

This is similar to planting a tree and later enjoying its fruit — season after season, year after year.

Why this ‘Plan for Life’ which is SIP + SWP strategy works effectively?

You gain financial independence because you decide how and when your income arrives.

SIPs, especially in equity mutual funds, can deliver returns that beat inflation. This helps your SWP payouts stay relevant and effective over time.

The structure is tax efficient. Only the withdrawn amount is taxed, and long-term equity investments enjoy favourable tax treatment.

You can avoid emotional investing. Since your income is planned, you do not need to sell in panic during market dips.

Your future does not need to rely on someone else signing your paycheck.

By starting your SIPs today, you are creating the foundation for your SWPs tomorrow. You are building your own self-funded,

self-sustaining monthly income.

True financial freedom is not just about creating wealth. It is about having the confidence that your next paycheck is already taken care of.

Disclaimers:

SIP does not assure a profit or guarantee protection against loss in a declining market.

An investor education and awareness initiative by Aditya Birla Sun Life Mutual Fund.

All investors have to go through a one-time KYC (Know Your Customer) process. Investors to invest only with SEBI registered Mutual Funds. For further information on KYC, list of SEBI registered Mutual Funds and redressal of complaints including details about SEBI SCORES portal, visit link : https://mutualfund.adityabirlacapital.com/Investor-Education/education/kyc-and-redressal for further details.

The information herein is meant only for general reading purposes and the views being expressed only constitute opinions and therefore cannot be considered as guidelines, recommendations or as a professional guide for the readers. The document has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Recipients of this information are advised to rely on their own analysis, interpretations & investigations.

Readers are also advised to seek independent professional advice in order to arrive at an informed investment decision.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.